Canadian M&A outlook for 2022

On its face, record-breaking M&A levels in Canada in 2021 appear to be setting the stage for an eventful year in dealmaking in 2022. However, deal activity is only part of the story of 2021 for dealmakers in Canada.

With continued economic volatility, and with Canadian businesses and industries being rapidly transformed by a number of developments (including technology and ESG factors, to name a few), M&A in 2022, much like the year before, will be shaped by a diverse range of drivers.

Canadian domestic deal activity

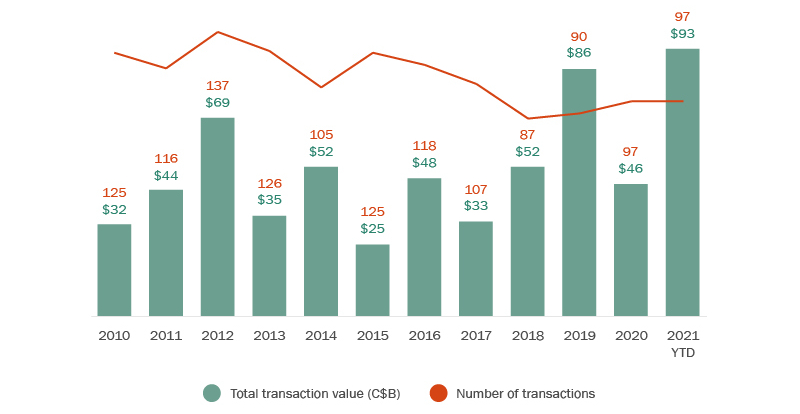

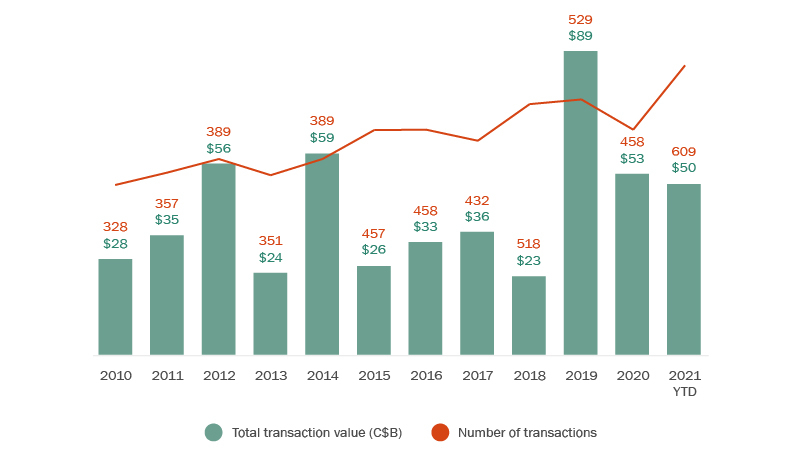

2021 was a blockbuster year for public M&A activity in Canada, with aggregate deal values reaching a 10-year high of C$93 billion (Figure 1). Transaction activity was driven by large-value transactions as a number of Canadian businesses undertook strategic transactions that underscored the confidence of boards and CEOs in this active deal environment. Sizeable Canadian transactions included Rogers Communications Inc.’s proposed C$26 billion agreement to acquire Shaw Communications Inc.1 and Brookfield Infrastructure Partners’ recently completed strategic acquisition of Inter Pipeline (valued at approximately C$14 billion).

Figure 1: Canadian public M&A market

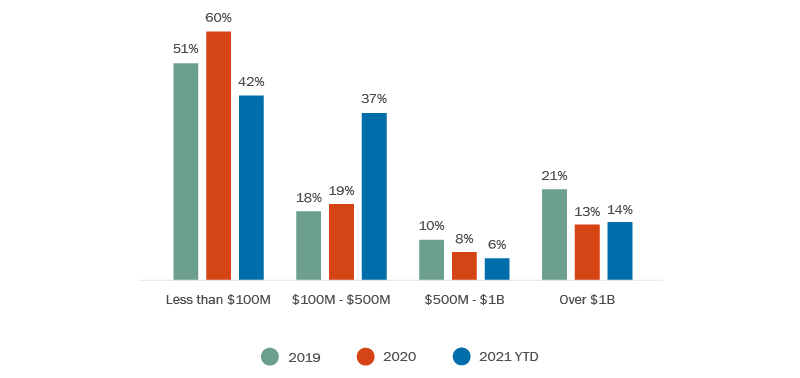

Meanwhile, deal activity in the mid-market segment (for transactions valued between C$100 million and C$500 million) grew significantly by 18% (Figure 2). Transactions valued up to C$500 million accounted for 75% of overall Canadian public M&A deal activity, in line with historical levels where mid-market deal activity has traditionally accounted for the majority of Canadian public M&A transactions.

More spin-offs and divestitures

While much M&A activity has stemmed from companies’ active pursuit of growth strategies, we expect to see, amid high valuations, market volatility and focus on strategic optimization, more businesses undertaking spinoff transactions and divestitures in 2022 as a way to return value to shareholders and refocus their strategic direction. For example, H&R REIT recently announced a strategic repositioning plan to transform from a diversified REIT into a simplified, growth-orientated REIT. As part of its plan, it will spin-out its properties under Primaris the Canadian retail division of H&R REIT, and, together with Healthcare of Ontario Pension Plan (HOOPP), create a new stand-alone, publicly traded REIT focused on owning and managing enclosed shopping centres in Canada2. In another example, George Weston Limited recently announced that it had signed a definitive agreement to sell its Weston Foods fresh and frozen bakery businesses to affiliated entities of FGF Brands Inc. (FGF) for aggregate cash consideration of C$1.2 billion3.

In what some are calling a bellwether move, GE recently announced its plans to spin off its healthcare, renewable energy and power companies to create three public companies4. GE Chairman and CEO H. Lawrence Culp, Jr. explained that, “By creating three industry-leading, global public companies, each can benefit from greater focus, tailored capital allocation, and strategic flexibility to drive long-term growth and value for customers, investors, and employees”.

Many spinoff and divestiture transactions follow investor demands that companies consider optimizing their business portfolios by separating, for example, high-growth businesses from low-growth businesses or moving similar sets of assets into distinct publicly traded entities with the expectation that they will each benefit from more focused management and investor interest as a stand-alone company.

Investor focus on business strategy

Another similar trend is investors becoming more vocal in pressing boards of directors and management of public companies to consider changes to corporate strategy and direction. For example, UK based hedge fund TCI launched a proxy contest involving CN Rail following its effort to acquire Kansas City Southern5. In another example, in May 2021 Dye & Durham Limited formed a special committee of its board of directors in response to an indication of interest to take the company private from a shareholder group led by management6. In October, the special committee concluded its review of current strategy and possible alternatives and recommended that Dye & Durham continue to pursue its existing business strategy which contemplates further growth through acquisitions7.

As valuations remain high and market volatility creates potential challenges to price deals, it may become more challenging for some boards to pursue M&A transactions. While market conditions are likely to remain uncertain, we expect shareholders will nonetheless continue to assert their views with boards and management on issues such as deal pricing and strategy—as well as other governance considerations such as ESG (which we cover in greater detail below)—in the year ahead.

Deal terms in focus

World events continue to impact deal terms in Canada and we have observed three notable developments that have shaped transactions in 2021. The pandemic triggered heightened focus on material adverse effect (MAE) termination provisions and interim operating covenants, as circumstances changed risk dynamics between signing and completion of transactions, leading parties to test the scope and nature of these provisions. In 2021 the courts in Duo Bank and Cineplex provided important guidance on MAE conditions and ordinary course covenants. They confirmed that the hurdle to prove an MAE is high, underscoring the importance of the specific terms of parties’ M&A agreements, particularly expressly stated exceptions. While Duo Bank and Cineplex will no doubt bear careful consideration by any party seeking to assert an MAE in the future8, as we enter year three of the pandemic, it seems unlikely that we will see a flood of MAE cases on the basis of COVID-19 specifically.

More and more, ESG is affecting virtually every aspect of M&A transactions and a driver of deal activity, as businesses look to reduce their carbon footprint and are developing targets and strategies to help achieve net-zero emissions and other related goals. ESG factors are now being seen as critical value drivers for dealmakers, as well as essential indicators of corporate values and reputational expectations. Effective diligence, evaluation and management of ESG considerations are therefore crucial steps in today’s M&A environment for parties to mitigate risk, achieve beneficial outcomes and synergies, and successfully execute transactions. Parties should take care to work through ESG factors early on and consistently—from the initial screening of opportunities to diligence, valuation and financing processes and through to execution, management of stakeholder expectations and post-deal integration9.

Finally, privacy and cybersecurity considerations are now more than ever business-critical aspects of the due diligence process of M&A transactions in the face of ongoing global privacy reform, the commercial value of personal information, and a consistent stream of cybersecurity threats. The buyer’s review of the seller’s privacy and cybersecurity management will inform the types of representations, warranties, covenants, and other rights or obligations that will need to be included in the M&A agreement.

Figure 2. Deal value ranges for acquisitions of Canadian public targets

Sector shifts

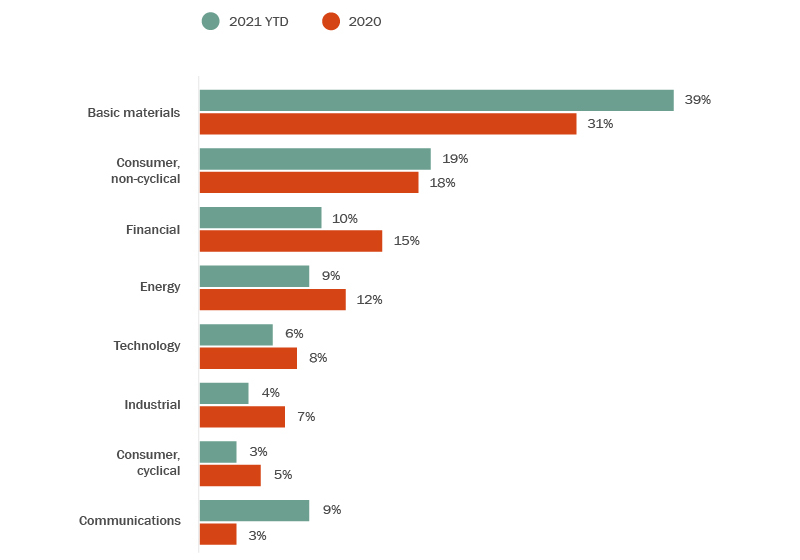

The basic materials, consumer and financial sectors attracted the most deal activity in 2021 (Figure 3). After facing headwinds, Canada’s oil and gas industry witnessed a decline in deal activity in 2021, though improving commodity prices and a more positive outlook point to renewed optimism for the oil and gas sector for the year ahead.

At the same time, the volume of deal activity in Canada’s mining sector has grown significantly in the last year, buoyed by strong commodity prices and new drivers of investment and transaction activity. Several significant transactions have continued the consolidation theme in the gold space, buoyed by strong gold price and the need for the major players to achieve growth and replenish reserves. The momentum to make and deliver on ESG commitments and the global energy transition is notably influencing investment in the sector. Of particular significance is the growing global trend toward electrification (including with respect to electric vehicles), which is leading to increased investment activity in “battery metals”—including copper, nickel, cobalt, lithium and graphite—such as Zijin’s pending C$960 million acquisition of Neo Lithium10. Altogether, these developments underscore the transformation that is underway in Canada’s vibrant mining sector, which enters 2022 in a position of strength.

In the financial services sector (which includes real estate), deal activity across a number of areas was strong in 2021, including in asset management, payments, fintech, insurance, banks, loyalty partnerships, and international bancassurance. The positive deal momentum in the financial services sector is set to continue in the year ahead, with the most recently released 2022 Bank Director M&A Survey showing that over half of the respondents view M&A as an important piece of their institutions’ growth in 2022.

Figure 3. Public M&A industry breakdown

Canadian cross-border M&A

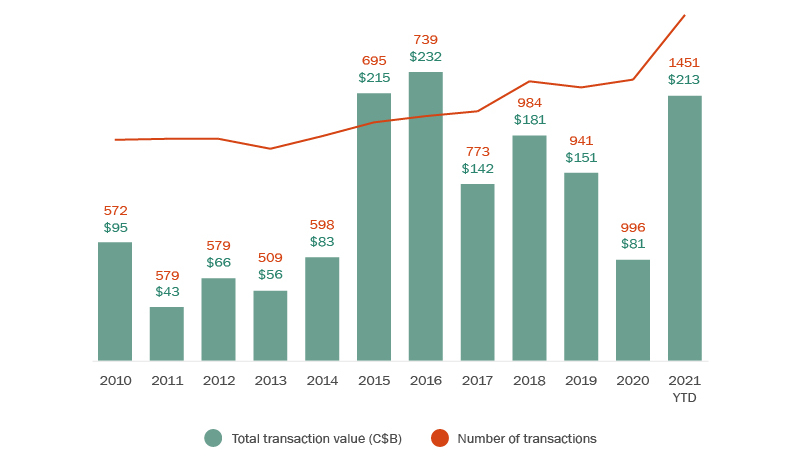

In 2021, Canadian outbound M&A activity reached a five-year high in terms of total deal count and aggregate transaction value (see Figure 4). The growth in deal activity has notably been driven by the increase in the acquisition of U.S. targets, which accounted for 60% of overall outbound deal volume in 2021.

Figure 4. Canadian outbound M&A activity

Access to larger markets and the pursuit of global scale were some of the key considerations driving outbound deal activity for strategic and institutional investors this year. One notable example was CN’s proposed US$33.6 billion merger with Kansas City Southern to create a groundbreaking North American railway connecting ports and rails across the United States, Mexico and Canada11. Another example was the US$1 billion acquisition by Constellation Insurance Holdings, Inc., backed by institutional investors Caisse de dépôt et placement du Québec and Ontario Teachers' Pension Plan Board, of Cincinnati-based Ohio National Mutual Holdings, Inc.—an established and diversified insurance carrier with a nation-wide footprint—to grow Constellation’s platform12.

After the disruption of the pandemic, and as many organizations continue to carry on remote operations, the technology sector is a particularly hot sector for cross border investment, as technology companies look abroad to expand. One example is Dye & Durham’s proposed C$3.2 billion transformative acquisition of Australian data services firm Link Group, the largest cross border acquisition by a Canadian technology company in 202113. The role of technology cannot be overstated for companies, especially those in retail and other areas where a digital presence is paramount for success. We are seeing the pull from all industries to integrate tech into their businesses resulting in exponential growth and investment opportunity for the Canadian tech sector.

Meanwhile, the aggregate value of foreign investment in Canada stayed largely on par with the last year, though deal volume increased by over 30% year-over-year (Figure 5). The U.S. remains the largest inbound source of foreign investment in Canada.

Figure 5. Foreign buyers of Canadian targets

Conclusion

With no signs of slowing down, deal activity in Canada is expected to continue its busy pace into 2022. At the same time, the protracted disruption of the pandemic alongside other technological and climate-related developments, as well as further guidance from courts and regulators, remain forces in play that will undoubtedly have knock-on effects on dealmaking. It will be interesting to see how the markets continue to respond to these widespread—and in many cases, worldwide—pressures in the year ahead.

- Torys is representing Rogers Control Trust on this transaction.

- Torys is acting as counsel to HOOPP on this transaction.

- Torys is acting as counsel to George Weston Limited on this transaction.

- See GE press release.

- Torys is acting for CN Rail in connection with proxy contest.

- See Dye & Durham announcement dated May 31, 2021.

- See Dye & Durham announcement dated October 8, 2021.

- Read more about these decisions in 2021 commercial litigation year in review and Big screen blues: Cineplex ruling sheds new light on pandemic MAEs.

- Read more in The growing importance of ESG in M&A transactions.

- Torys is acting as counsel to Zijin.

- Torys acted as counsel to CN.

- Torys acted as counsel to CDPQ and Ontario Teachers’ Pension Plan Board.

- Torys is representing Link Group in Canada on this transaction.

To discuss these issues, please contact the author(s).

This publication is a general discussion of certain legal and related developments and should not be relied upon as legal advice. If you require legal advice, we would be pleased to discuss the issues in this publication with you, in the context of your particular circumstances.

For permission to republish this or any other publication, contact Bryn Turnbull.

© 2026 by Torys LLP. All rights reserved.

Tags

Transactions

Advisory and Regulatory

M&A

Capital Markets

Private Equity and Principal Investors

Sustainability

Board Advisory and Governance

Financial Services

Infrastructure Energy and Resources

Mining and Metals

Infrastructure

Oil and Gas

Technology

Media and Communications

Government and Crown Corporations

Cybersecurity

Competition and Foreign Investment Review