Buyers Will Find New Ways to Gain an Edge in Private Company Auctions

Authors

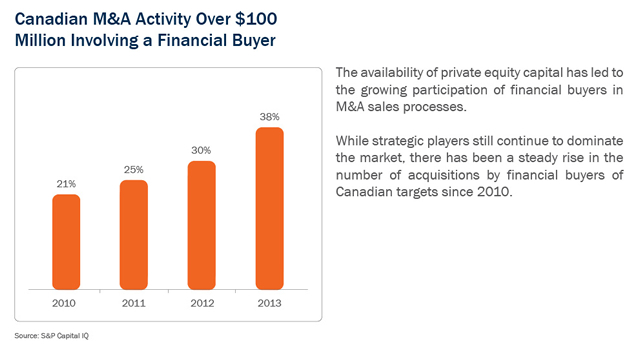

Competition for proprietary deals, coupled with the availability of private equity capital, has led to increasing numbers of financial buyers participating in organized sales processes to originate deal flow. Prospective buyers in competitive auctions for private companies continue to push the boundaries to achieve an advantage in this environment – a trend we expect will continue in 2014.

On the buy-side, every competitive auction appears to be attracting a significant number of private equity firms, especially U.S.-based firms. The U.S. firms and their Canadian competitors are increasingly using industry specialization to differentiate themselves – not just through research, but often through investments in sector-specific companies and, in some cases, through establishing in-house operations teams. The result is that these financial buyers can match strategic players with deep industry insight and, with this confidence, they are often prepared to bid up the price or accept more post-closing risk. These new hybrid financial/strategic buyers are squeezing out other private equity firms without the same specialization and are competing more effectively against strategic buyers. Since they are also better positioned to partner with other industry players, make ambitious business plans more realistic and provide greater value through strategic planning and operational improvements, they can ultimately support higher purchase prices for businesses.

Timing and certainty of closing are other factors that potential buyers are using to differentiate themselves in a competitive bidding environment. A firm with industry expertise and a strong track record of closing deals and creating value in the relevant sector can increase a seller’s confidence in that firm’s bid in terms of both the bidder’s ability to execute the transaction and its ability to carry the business forward post-closing. This will be particularly important to sellers rolling a portion of their equity into the acquired business. Firms planning a combination with an existing investee company have the added advantage of third-party financing sources already in place, which usually increases certainty and reduces the time to closing. Sellers are also working to improve the efficiency of the bid process and ensuring the completeness of bids submitted during the auction. They are, for example, prepackaging key due diligence matters to fully educate buyers on inherent risks associated with the business being sold and to facilitate timely bids that are less conditional on, or subject to, price renegotiation pending due diligence review.

In some circumstances, buyers have attempted to gain a timing advantage by pursuing transactions on an immediate “sign-and-close” basis, without an interim preclosing period that would ordinarily be used to obtain regulatory approval of the deal. Efficient sign-and-close transactions require a preliminary determination that regulatory approval is perfunctory. Buyers that have arrived at that assessment may initiate the regulatory process at their own cost in advance of a signed deal to allow for immediate signing and closing of the transaction once regulatory approval is obtained. This approach also helps avoid unnecessary friction with management that may come from negotiating a suite of interim operating and other protective covenants designed to safeguard the buyer’s interest in the transaction pending closing.

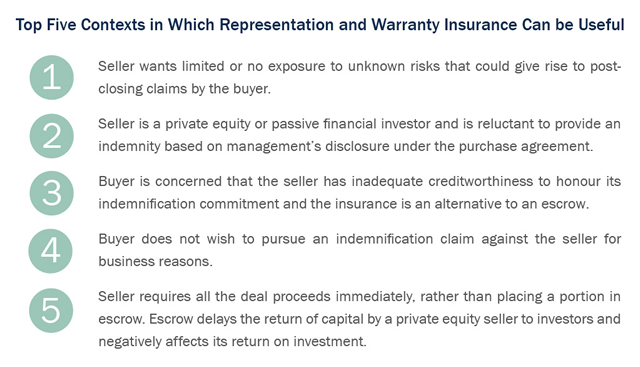

Some prospective buyers are also seeking to increase their chances at successful bids through representation and warranty insurance. A buyer can purchase a policy to cover indemnity claims for breaches of representations and warranties in a purchase agreement. This coverage is relatively inexpensive – typically a one-time premium of 2% to 3% of the coverage. Without reducing the buyer’s indemnification coverage, the insurance allows a buyer to reduce its indemnification demands on a seller, including reducing the need for a portion of the sale proceeds to be held in escrow. It has the added benefit of preserving goodwill with management by reducing the need for buyers to possibly pursue claims against sellers, who often remain on the management team after the change of ownership.

Although representation and warranty insurance has been available for many years, interest in the coverage is growing. This tool, along with the specialization of financial buyers, prospective buyers’ focus on tightening timing and the closing certainty on transactions, will affect private company auction dynamics in the year to come.

To discuss these issues, please contact the author(s).

This publication is a general discussion of certain legal and related developments and should not be relied upon as legal advice. If you require legal advice, we would be pleased to discuss the issues in this publication with you, in the context of your particular circumstances.

For permission to republish this or any other publication, contact Janelle Weed.

© 2024 by Torys LLP.

All rights reserved.